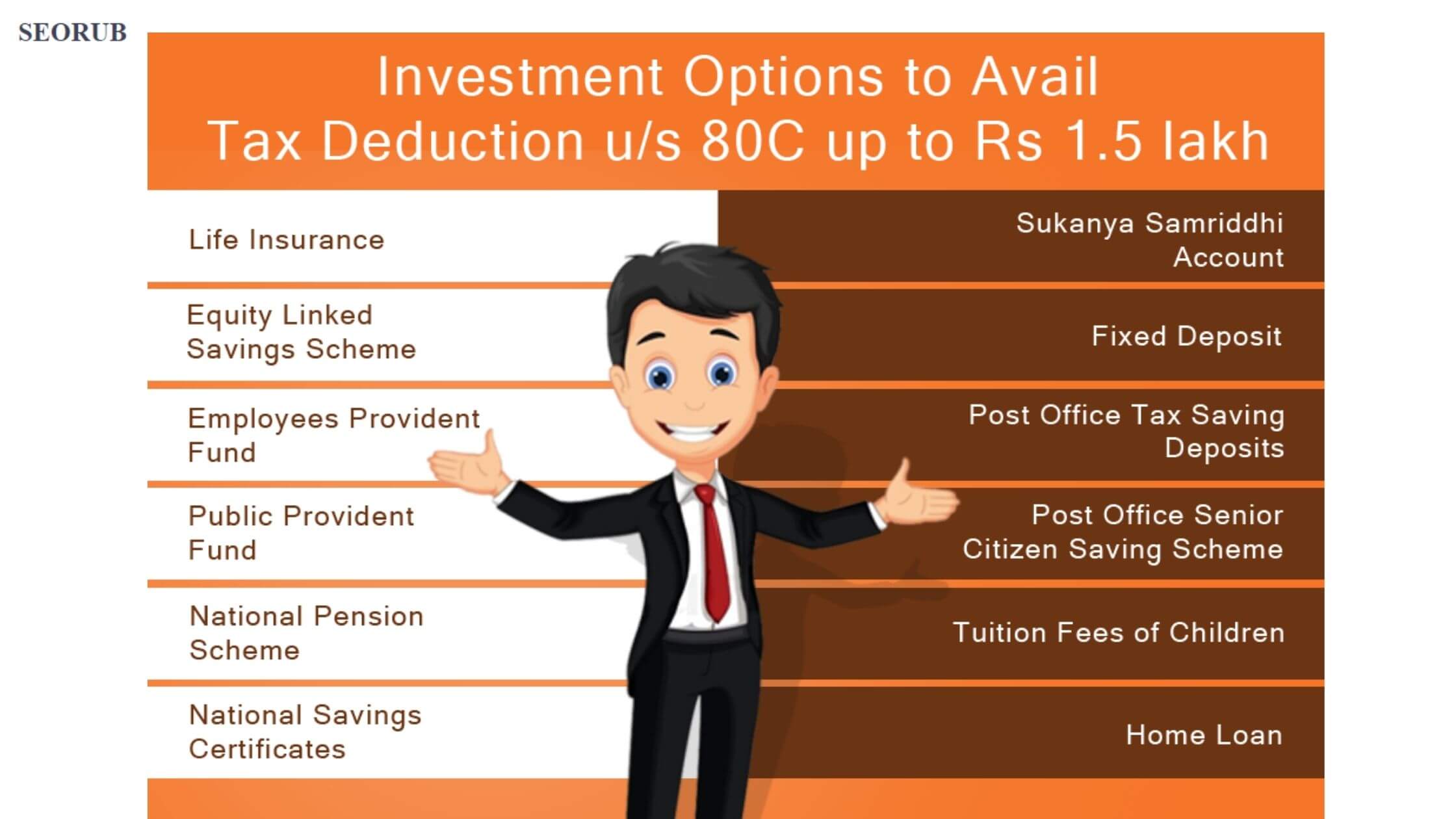

Intro of Section 80C limit

Last year, Finance Minister Arun Jaitley raised the Section 80C limit for mutual funds from $15 million to $20 million per fund per quarter. Now that the Budget is out, over 5 lakh investors are waiting to know whether he will raise the cap in this year’s budget.

Possible explanation for this might be simple: it is unclear whether Finance Minister Arun Jaitley will raise the cap in this year’s budget. But there are also a couple of reasons why investors might not be expecting it.

First, there are some areas where the finance minister has done little or nothing to change rules and regulations. For instance, he did not stop investors from investing more than the limit on income-oriented funds and did not do anything about tax-saving schemes like tax deduction of capital gains.

Second, by raising the cap on mutual funds at a time when government is planning to introduce new tax measures and reforms that could affect investors’ returns may have put a dampener on investors’ expectations.

Third, some of his decisions may have been in favour of existing players who invested a lot in earlier years but did not own more than $15 million per fund (the current limit).

Maybe that shows how important it is to look at old investments and make sure they get treated as good investments because they are valued high today. So what impact would raising the cap have?

What is Section 80C of the Income Tax Act?

80C limit is a tax saving that allows some taxpayers to avoid paying income tax if they invest in securities classified as equity-linked securities (ELSS). Section 80C was introduced during the last financial year back in 2010 as a temporary measure. It was intended to help middle income taxpayers save on their income tax liability.

The exemption is available only to investors who were not earlier eligible for the exemption and who make contributions to equity linked savings schemes (ELSS) and other equivalent savings schemes.

There are two types of ELSSs: domestic direct investment (DIL) and offshore direct investment (ODI). DIL means investments made through a direct investor’s local bank or other financial institution. ODI means investments made through an offshore entity such as an Asian/Pacific International Investment Company (APICORP).

Investments in DILs and ODI are paid benefits of employment rights, pension plans, statutory retirement benefits, social security contributions and employer’s contributions.

Investments in non-dilatable securities are taxed at the applicable tax rate. However, where taxation is due on capital gains arising from such investments, the levy of tax will depend on the character of security held by the taxpayer.

The threshold for qualifying for Section 80C benefit is set at Rs1 lakh per annum for individuals who are not residents of India or those subject to income tax at source but have an annual taxable income exceeding Rs5 lakh or whose total taxable income exceeds Rs20 lakh per annum; it is Rs10 lakh per annum for individuals who are residents of India or those subject to income tax at source but have total taxable income exceeding Rs20 lakh per annum.

It is also Rs4 lakh per annum for head of family with total taxable income exceeding Rs20 lakh per year. The maximum benefit which can be received under this section will be 50% of annual salary up to the limit which cannot exceed $2 million.

How to Save Tax under Section 80C?

Probably the most famous part of Section 80C is the fact that it exempts “anybody investing in any funds or schemes registered with the Securities and Exchange Board of India (SEBI) from paying any tax on the amount invested in such funds or schemes.”

The phrase “registered with SEBI” is key. You see, there are two types of fund schemes: open-ended funds and closed-end funds. A closed-end fund is a fund which has been established by an individual (who can be a company, etc.). For example, you put money into an ISA (Individual Savings Account) to save for your retirement. When you withdraw your money at retirement, you owe income tax on it.

Open-ended funds are popular because they allow investors to take a piece of every fund they invest in. You buy shares in a stock market index fund, which then buys stocks from other investors’ portfolios. This means that if one investor buys 100 shares of Apple Inc., he will not pay tax because he only bought into one share within the index. This can be a powerful tool for those with small investment amounts who don’t want to worry about taxes.

However open-ended funds do have their drawbacks as well. An open-ended fund is not transparent — and that’s why we use Section 80C as a way of avoiding taxes on profit made from trading stocks rather than just investing directly into stocks directly.

Another drawback of open-ended funds is that they have no long term goal beyond the current year — and if you were to lose money over the course of your life, you may end up paying a lot more tax than you would if you had put all your money into an index fund!

In addition to these downsides, there is another problem that can occur when investing in open-Ended Funds: When one company goes bankrupt or shuts down its operations, its assets will be transferred to another company which has also registered under Section 80C; but this new company will not pay taxes on those assets anymore! So even if it makes money (and so does SEBI), it still has no incentive to make profits and continues to invest for years! So basically, this means that those who invest money in closed end funds do so with the knowledge that their investments could easily disappear before they reach retirement!

So yes, I know all this sounds quite mysterious; but trust me when I say this: It’s about time we start taking our accounting

Equity Linked Savings Schemes (ELSS) – The Best Option Under Section 80C?

The Finance Ministry is expected to present an ambitious plan for the ongoing fiscal year. The Finance Minister, Arun Jaitley, has been quoted as saying that the government will increase the limit for equity linked savings schemes (ELSS) from Rs 1.5 lakh crore to Rs 2.5 lakh crore.

But is this the right direction? Can Equity linked Savings Schemes (ELSS) be a viable option under Section 80C of I-T law?

Analysing ELSS and other options under Section 80C, it looks like they are not as well suited to small investors as we had assumed they would be. But that doesn’t mean they don’t have a place in the shadow banking system or in tax-saving schemes like LTCM funds and I-T mutual funds. The total corpus raised by ELSS schemes in FY17 was just Rs 3,700 crore ($591 million), which would be around 5% of their total corpus raised in FY16 and 4% of their total fund raising capacity for FY17. ELSS schemes are also subjected to more scrutiny than other tax saving instruments because their return is determined by the performance of mutual funds that invest solely in these schemes (the fund’s performance will account for 15% of its corpus).

But there is another advantage: equity linked deposits can’t be tapped easily under Section 80C, while equity linked savings schemes can be cash deposited into them (which means one can withdraw them at any time).

This has led some people to argue that equity linked savings scheme might actually be a better option for small investors than 80c limit based on these grounds alone.

Use cases in which ELSS have been used include:

• A company with very low gross profit margin gets 15% capital gains every year from selling assets if its net profit margin exceeds 30%. So increasing its income by 5%, it could raise up to Rs 70 crore from selling assets every year using 80c limit limits .

• A healthcare facility required money from donors once a month during winter season, with an annual cap of Rs 20 lakhs per donor and use this amount only once per month against conditions laid down by donors; so it takes out loans against assets worth above Rs 20 lakhs and use it only once per month against conditions laid down by donors.

Investment Options under Section 80CCF – The NPS and the Cont

If you are an existing (almost) non-registered mutual fund investor, you do not have to pay tax on the gains in your investment.

There is a lot of confusion about Section 80C and the NPS. It may be that most people only know that they do not pay tax on the net capital gain (after deduction of any capital losses) but they don’t know whether they will also get a bonus or not. That’s because there is no limit on how much you can invest in such schemes as long as you invest more than ₹1 lakh per annum without any tax consequences.

For most people, it makes sense to contribute tax-free, so long as your investment has a market value of ₹1 lakh or more. But what if you want to invest as little as ₹10,000 a year? Your best bet might be to look at investing in a mutual fund which offers low-cost equity instruments in the NPS or through public provident fund schemes such as Public Provident Fund (PPF).

If you are new to investing, and are just looking for places where you can put your money, then it would be best for you to avoid these schemes altogether. You would need to look at other options such as regular shares, mutual funds and bonds or exchange-traded funds (ETFs).

One of the main reasons for investors avoiding these schemes is that their initial investment is tax-free. So if you invest money into such schemes from April 1 onwards, there will be nothing stopping you from taking out profits and withdrawing them till June 30 next year (which is why many investors are opting for short term investments).

More from my site

Grindwell Norton Share Price Live (2,093.00 INR): Investors Analysis

Grindwell Norton Share Price Live (2,093.00 INR): Investors Analysis- Green Dot Bank: A New Way to Bank

- Bollinger Bands: What They Are and How They Work

- TradingView Export Data & Download Data into CSV File: How to Export Chart Data and Strategy Data from TradingView?

- Tradingview Custom Screener Script: How to Setup and Use It for Best Results

- 16 Standard Colors of Pine Script of Tradingview